Repricing Exuberance, Part I

Silicon Valley's Biggest “Half-Off” Sale Is Just Getting Started

Summary: Many late-stage VC-backed tech startups are still marked at unrealistic valuations. The past year has been tough, but we haven't seen the bottom yet — there is more pain coming. Most founders and VCs have tried to avoid marking down their companies, but over the next 6-18 months they will have no choice. Even well-funded companies are starting to run out of cash, and eventually many will have to:

raise a “down” round at a much lower valuation, or

accept a pressured acquisition (again, at a lower valuation), or

shutdown entirely (new valuation = ZERO)

As this happens, typical late-stage company valuations will get cut in half. As a result, there will be excellent opportunities to buy or invest in [some] good companies and funds at greatly reduced prices. Silicon Valley is going on sale — prudent shoppers grab your checkbooks.

Note: Mostly this piece is just me re-hashing a more thoughtful post by Elad Gil written in Feb 2023. If you have time, ignore my BS below and just go read his stuff (and many other great posts). Elad also has way more data and colorful charts. However if you don’t have time, here’s the punchline:

source: Elad Gil, Startup Decoupling & Reckoning

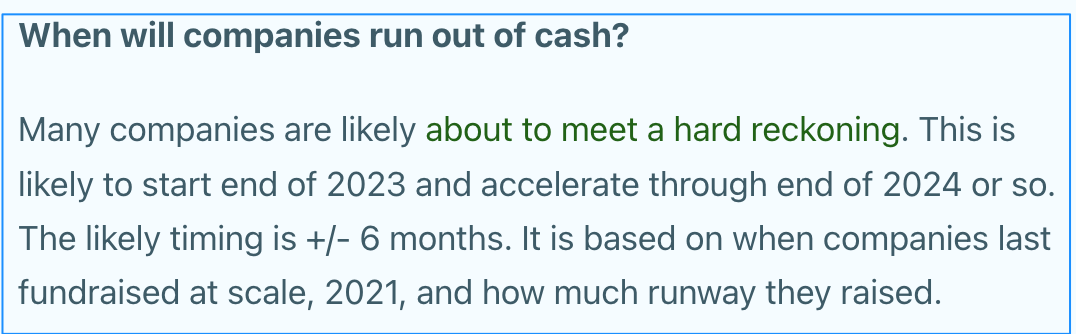

Elad predicts that many later-stage tech startup valuations will re-set substantially in the next 12 months. While the exact timing is debatable, there is no question we haven’t seen the worst of this yet, and we are likely to see a significant wave of markdowns that starts happening sometime around the end of this year.

BUT WAIT DAVE — is this really news? Hasn’t this already happened?

Well, currently most private tech companies are still “officially” held at rather lofty valuations by both VCs and entrepreneurs. Especially for companies that had enough cash to avoid raising capital in the past 18 months, they have tried to cut their burn, improve their economics, and grow into and justify previous optimistic marks. But as their cash runway gets shorter, these companies will face tough decisions that will require difficult new financings, desperate acquisitions, and in some scenarios even company shutdowns.

These mark-to-market events will inevitably force new and lower valuations far less exuberant than during the ultra-low interest rate era of 2020-21. The over-valuation party for public companies ended in Q1 2022, but the private market is only just now waking up to a re-pricing hangover that will come crashing down thru the end of 2023 and into 2024.

Another factor driving lower valuations is the need for liquidity by investors. Since there haven’t been any notable tech IPOs in the past 18 months — and there don’t appear to be any new ones on the horizon yet — tech investors haven’t seen much cash coming back for quite some time. And there are also several large VC portfolios up for sale: SVB Capital, FTX Ventures, and now Tiger Global are all in the process of unloading a number of investments in VC funds and companies. That’s a hell of a lot of inventory for the market to absorb in such a short time, and sellers who want short-term liquidity will be at a significant disadvantage.

Many companies (and funds) are going to be available at much lower prices than at any time in the past decade. Already several companies on secondary marketplaces like Forge and Equityzen are priced at significant discounts to their last round valuations, with far more sellers than buyers.

For investors and acquirers with ready capital available, Silicon Valley is about to witness its biggest half-off sale in over a decade. Smart buyers should do their homework and be prepared to grab a bunch of tech startup bargains.

(next up in Repricing Exuberance Part II: find out why VC fund secondary opportunities are even better bargains than direct company secondary sales…)

Excellent insights Dave. VC investment is the early signal to market direction. Watch what they do, not what they say. VCs want to preserve the valuations of their portfolio companies, and will say optimistic things. But, watch how they invest new dollars for the real story. Same with Founders. They want to preserve their valuations, but watch how they hire or layoff for the real story.

Looking forward to more posts from you and @amanpvc :) He IS a top LinkedIn Financial voice you know…